Every few months, economist Roelof Botha publishes a look at how South African households are really doing financially, using data most of us never see. It comes wrapped in the usual economic language: indices, basis points, real versus nominal growth. Strip that away, though, and there's a simple story underneath that matters to anyone with a bond, or hoping to get one: are interest rates helping or hurting right now, and what should that mean for how you think about buying or paying off property. Here's what the latest numbers actually say, and what they mean if you own a home, or want to.

Household finances are improving, and it's mostly about interest rates

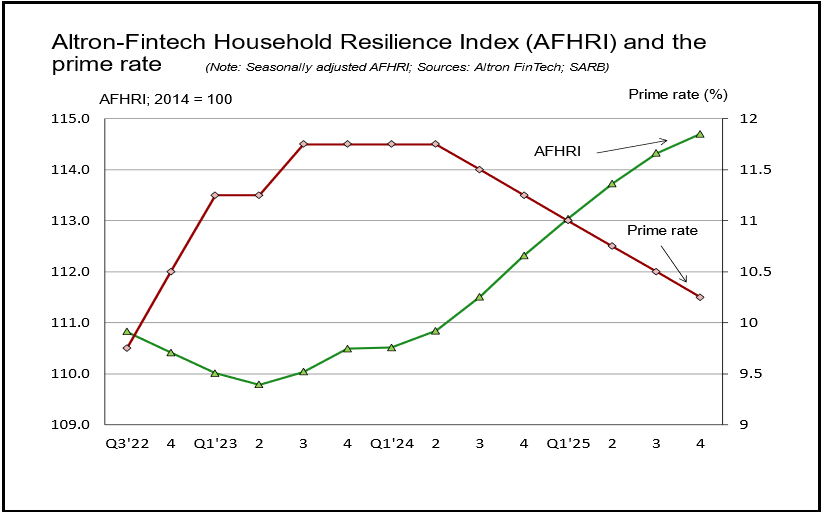

Twice a year, an index called the Altron FinTech Household Resilience Index measures how much financial breathing room South African households have. Think of it as a scorecard for whether people are managing better or worse than before. The latest reading, released in June, showed its seventh straight improvement in a row, sitting 14.7% above where it stood back in 2014, and up 2.2% on the year before.

The main reason: lower interest rates. When rates come down, servicing debt costs less, so the ratio of household income to debt costs improved by 7.1% year on year, leaving families with 4.1% more to spend on everything else.

This index moves like a seesaw against the prime lending rate, South Africa's benchmark rate for loans, including most mortgages. When prime dropped to a rock-bottom 7% in mid-2020 during Covid, the resilience index jumped more than 9% almost immediately. When prime later climbed to its highest level in 15 years, that same resilience eroded, and now that rates are easing again, households are recovering. This isn't an abstract statistic. For anyone paying off a bond, it plays out directly in what's left in the bank account after the repayment goes off each month. Every percentage point cut to prime takes real money off that repayment; every hike adds to it.

Bonds are still growing in size, just more carefully

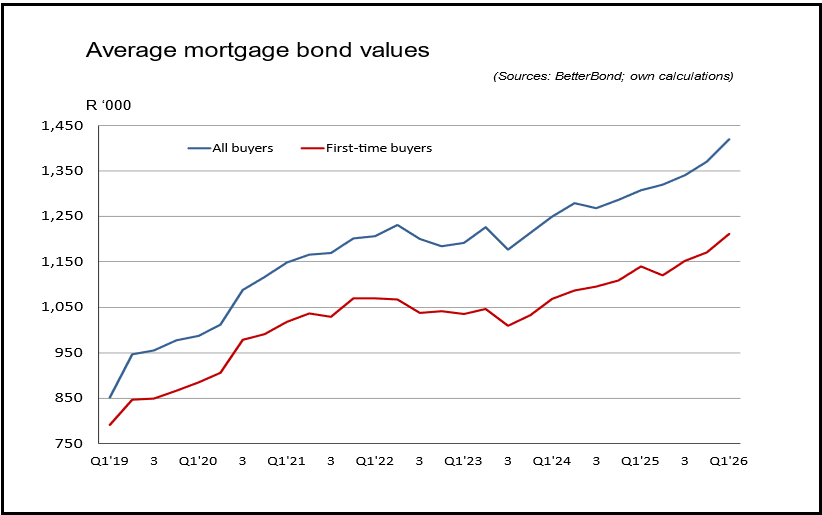

The average mortgage bond has grown by 44% since early 2020, based on figures from bond originator BetterBond. That sounds dramatic until inflation is stripped out. Once it is, real annual growth comes down to a modest 1.6% a year. In other words, bond values are rising mostly because prices generally are rising, not because people are borrowing dramatically more once inflation is accounted for. Part of why growth hasn't been faster is that banks keep adjusting how much deposit they want before approving a home loan. Since 2020, the average deposit required has gone up eleven times and come down six times, so banks have been tightening and loosening their lending criteria depending on how risky they judge the market to be at any given moment.

The biggest brake on the property market, though, has been the Reserve Bank's Monetary Policy Committee, the small group that meets several times a year to set the repo rate, which in turn determines the prime lending rate banks charge everyone else. In 2023, that committee pushed prime to 11.75%, the highest level in 15 years, even though there was little sign South Africans were overspending. The inflation at the time was mostly imported, driven by an oil price spike after Russia invaded Ukraine, not by excessive borrowing or spending at home. For anyone buying property, this is really a story about affordability on two fronts at once: how big a deposit needs to be saved, and how expensive the resulting bond repayment turns out to be. Both have moved unpredictably over the past six years, which is why it has felt like a genuinely bumpy market rather than steady growth.

A familiar pattern is playing out again, with reasons for cautious optimism

A war in the Middle East pushed oil prices up again, and the Reserve Bank responded by lifting prime to 10.5%. The encouraging part is that the conflict shows signs of easing, and inflation is cooperating: food prices, the single largest item in the basket Stats SA uses to measure inflation, are at their lowest level in 17 months, and diesel prices have already dropped by almost 20% since May. If that holds, it takes pressure off the Reserve Bank to keep hiking, and could open the door to further relief instead. For anyone with a bond, this is the pair of numbers worth watching, not the war itself, but oil and food prices, since those are the leading indicators for where a bond repayment is headed next.

Why central banks buying gold is not just a gold story

Elsewhere, central banks around the world, the institutions that manage countries' foreign currency and gold reserves, are still buying gold. A 2026 survey by the World Gold Council found that 89% of the central banks it surveyed expect global gold reserves to keep rising over the next year. That is slightly down on 2025 but still far above the sentiment seen in 2021, and most of these institutions, 74% of them, expect to hold less of their reserves in US dollars over the next five years.

This matters even to readers who will never buy gold, because it is a signal about global confidence in the US dollar and other traditional safe havens. When major institutional players quietly shift away from the dollar, it can affect currency stability worldwide, including the rand, and currency stability feeds directly into imported inflation on fuel and imported goods, which, as the previous section showed, is one of the main things that moves the prime rate.

What this means going forward

Put together, the picture is genuinely encouraging right now: cheaper debt, easing food and fuel prices, is filtering through into real relief for households and bondholders. But every part of this story, Covid, Ukraine, the Middle East, follows the same pattern. South Africa's interest rates are hostage to global shocks that happen well outside its borders: oil prices, wars, and shifts in currency confidence. The practical lesson for property owners and buyers isn't to try to predict the next shock.

It's to plan for both directions: enjoy the relief while rates are easing, but keep enough room in the budget to absorb the next unexpected hike, because the pattern in this data suggests there will be one. If it isn't clear how well your bond is positioned for that, that's worth a conversation before rates move again.