Every month, economist Dr Roelof Botha pulls together the numbers that really matter - interest rates, credit ratings, business confidence, trade data - and every month, those numbers eventually land on the desk of a bond originator trying to get a deal approved. This month’s data tells a more encouraging story than the headlines suggest. Yes, the Reserve Bank has tightened the screws again. But underneath that, South Africa’s fiscal credibility, business confidence and consumer spending power are all moving in the right direction. Here’s what it actually means if you’re buying a home, selling one, or helping someone do either.

The Prime Rate Hike: What It Means for Your Bond Repayment

The Monetary Policy Committee has pushed the repo rate up again, taking prime to 10.5%. For anyone on a variable-rate home loan, that’s a direct hit to the monthly repayment - and it tightens the affordability math banks use when assessing new applications.

The MPC’s reasoning is the global oil price shock triggered by the conflict in the Middle East, combined with South Africa’s own decision to abandon its old 3%–6% inflation target band in favour of a hard 3% point target. Several respected economists, Joseph Stiglitz among them, have argued that hiking rates in response to supply-side shocks like an oil spike does more harm than good to growth - but the MPC has gone the conventional route regardless.

- What this means for buyers: Your pre-approval just got a little harder to secure. Banks recalculate payment-to-income ratios every time prime moves, and a 10.5% rate eats into the loan amount you’ll qualify for. This is exactly the environment where a properly structured application - with the right supporting motivation, the right bank matched to your profile - makes the difference between an approval and a decline.

- What this means for agents: Buyer enthusiasm doesn’t always survive contact with a bank’s affordability calculator. Getting buyers pre-qualified before they fall in love with a property saves everyone time, and it’s worth leaning harder on that step while rates sit at this level.

Fitch and Moody’s Upgrade South Africa: A Vote of Confidence

Here’s the genuinely good news. Fitch Ratings lifted South Africa’s long-term credit rating a full notch, from BB- to BB, with a stable outlook attached - the first upgrade of its kind in over twenty years. Moody’s didn’t move the rating itself but upgraded the outlook, signalling it sees more good news on the way. South Africa is now one of only two G20 countries to receive a ratings upgrade from Fitch this year.

The driver is fiscal discipline: National Treasury’s budget tables show the country is sustaining a primary surplus (revenue exceeding non-interest spending), and Moody’s specifically flagged confidence in the Government of National Unity holding together and pushing forward on energy, logistics and water infrastructure - the kind of investment that crowds in private capital.

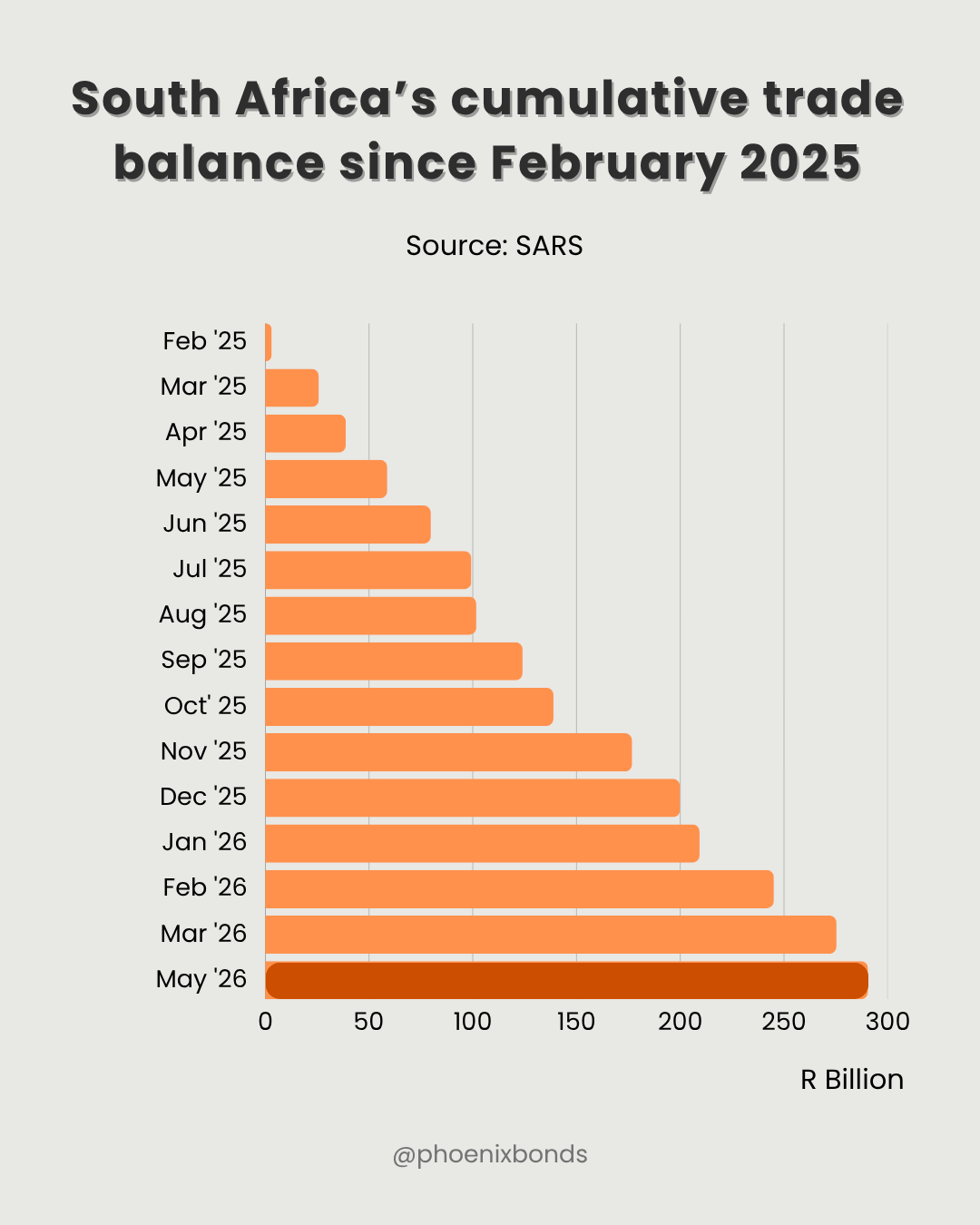

Although the trade surplus has moderated from its post-pandemic peaks, South Africa has continued to record positive trade balances. This has contributed to a more stable current account and strengthened investor confidence, supporting the recent improvement in the country's sovereign credit ratings.

Strong exports → Trade surplus → Stronger balance of payments → More foreign currency entering South Africa → Lower external risk → Better sovereign credit rating

What this means for property: Sovereign credit ratings sit upstream of everything else in the lending chain. A stronger rating lowers the cost at which government and, eventually, banks can borrow, which feeds through to mortgage pricing over time. It also makes South African property - residential and commercial - a more credible asset class for both local and offshore investors who use sovereign risk as a first filter. This is the kind of signal that, with a lag, supports property values rather than threatens them.

Business Confidence Is Building - and Confidence Buys Houses

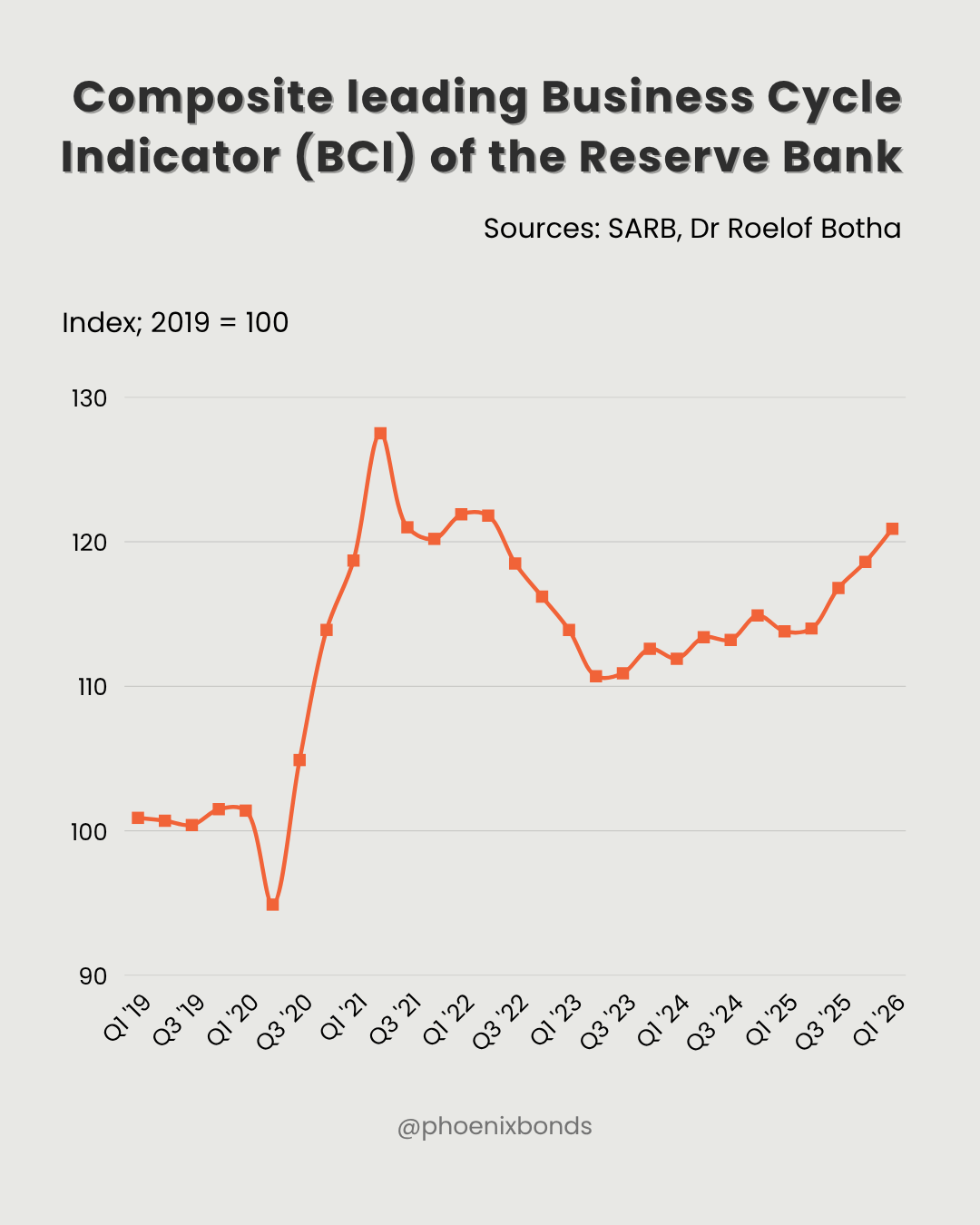

The Reserve Bank’s composite leading business cycle indicator rose 2.4% in March alone and 7.5% year-on-year, with six of its seven components moving positively - even as the equivalent indicator for our major trading partners declined. The standout contributors were stronger real money supply growth, a wider interest rate spread, record new vehicle sales, and a jump in job advertising volumes. That last point matters more than it sounds: record car sales and rising job ads are both classic proxies for household confidence. People don’t take on a car payment or post a job vacancy when they’re bracing for the worst.

This lines up with the Absa Purchasing Managers’ Index, which climbed to 52.6 in April - its best reading in 19 months - before easing slightly in May but holding above the neutral 50 mark. What this means for buyers and agents: Confidence is the fuel for property decisions. Buyers act when they feel secure in their income and their job prospects, not just when rates are low. A rising BCI and an expanding PMI both point to a buyer pool that’s more willing to commit, even with prime where it is. For agents, that’s a reason to expect more serious, qualified enquiries rather than pure window-shopping in the months ahead.

Wholesale Trade Is Booming - A Pulse Check on Household Spending Power

Wholesale trade sales broke a downward trend that had persisted since late 2023, posting 9.3% year-on-year growth in March and a striking 13.7% quarter-on-quarter jump - pushing total sales above R300 billion for the first time since the festive season rush of November last year. Nine of twelve wholesale categories grew, with food & beverages and machinery & equipment leading the pack. What this means for property: Wholesale trade is a useful early-warning indicator for the broader consumer economy. When wholesalers are moving more stock, it usually means retailers downstream are seeing stronger footfall and spend - which, in turn, supports the household income and savings position that underpins deposit-saving and bond affordability. It’s not a direct property indicator, but it’s a healthy sign for the household balance sheets that banks scrutinise on every application.

Final Thoughts: Reading Past the Rate Hike

If you only look at the prime rate, June’s data looks discouraging. But step back, and the picture is one of an economy quietly building credibility - a rare double credit rating endorsement, accelerating business confidence, and consumer-facing trade numbers that haven’t looked this strong in years. For buyers, the message is simple: tighter affordability at the bank doesn’t mean the door is closed - it means the application needs to be built more carefully, matched to the lender most likely to say yes, and supported by a clear motivation where your profile needs one. That’s precisely where a specialist originator earns their place in the transaction.

For estate agents, it’s a market where buyer confidence is real but bank approval is harder won. The agents who get ahead of that gap - by getting buyers pre-qualified early and partnering with an originator who can place the deals other originators can’t - are the ones who’ll close more transactions in this cycle, not fewer.