Analysis by Dr Roelof Botha | Commentary by Phoenix Bonds

At Phoenix Bonds, we read the economic data so you don't have to. Every quarter, economist Dr Roelof Botha publishes a "Silver Linings" report unpacking where the South African economy is heading. The May 2026 edition covers inflation, property market activity, bank lending health, and consumer spending - all of which directly affect your ability to get a home loan approved, and at what rate. Here's what it means for buyers, sellers, and estate agents on the ground.

1. Inflation is behaving - but there's a wildcard

South Africa's inflation numbers are, by most measures, in good shape right now. Consumer price inflation sits just above 3% and producer price inflation just above 2% - both comfortably within the South African Reserve Bank's target band.

The problem is geopolitics. The Strait of Hormuz - one of the world's busiest oil shipping routes, sitting between Iran and Oman - has effectively been closed to tanker traffic due to the ongoing conflict in the Middle East. That's pushing global fuel prices higher, and fuel prices feed into almost everything: transport, food, manufacturing, construction materials. If the situation doesn't resolve quickly, we could see SA's inflation tick upward in the months ahead.

Why does this matter for home buyers? Because the Reserve Bank uses the inflation rate to decide whether to cut or hold interest rates. The repo rate is currently on a cutting cycle - which is good news, as it brings down your home loan repayments. But if inflation picks up due to fuel costs, the Bank may pause or reverse those cuts. The compounding factor is that the SARB recently removed the flexibility it had around its inflation target range, meaning there's less room for it to look the other way if numbers creep up.

Bottom line: rates could stay where they are or improve further if the Middle East situation stabilises. Watch fuel prices as your leading indicator.

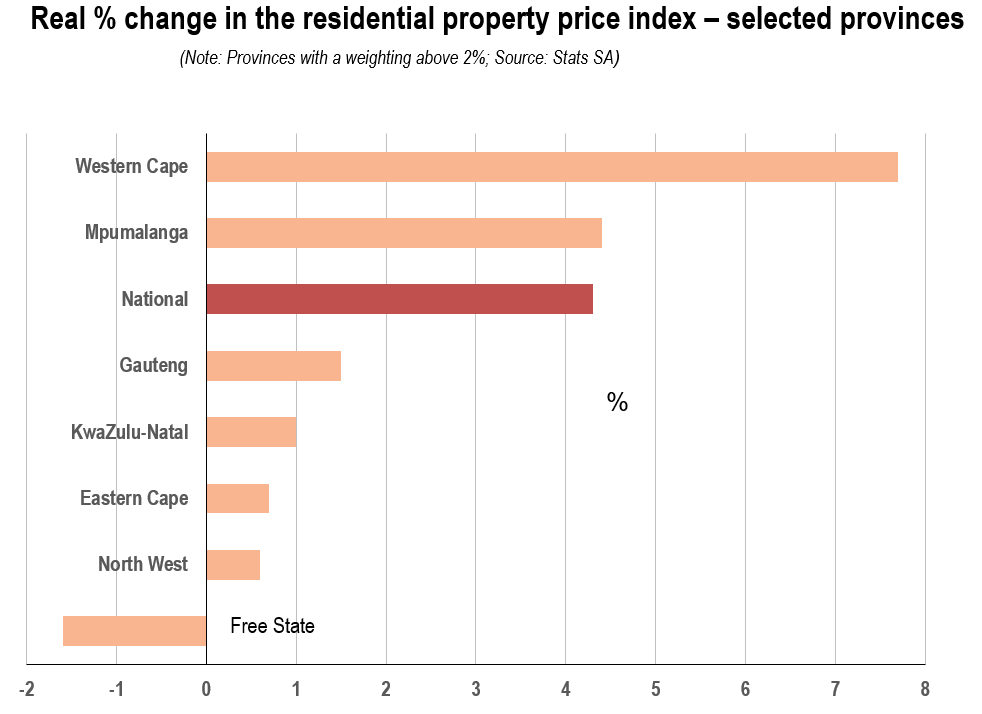

2. Gauteng and the Western Cape are where the market is

New data from relocation firm Wise Move and Statistics SA confirms what most estate agents already know: South Africans are moving - and they're overwhelmingly moving within Gauteng and the Western Cape. Together, these two provinces account for 89% of all tracked inbound and outbound relocations nationally.

The Western Cape is outperforming on price growth, with the Stats SA Residential Property Price Index (RPPI) showing real house price growth of 7.7% in 2025. BetterBond data puts the number slightly lower at 5.8%, but either way, the Western Cape is the only province posting meaningful real-terms growth. The Eastern Cape is also seeing a modest net gain from inward migration - a slow but notable trend.

Gauteng, meanwhile, dominates in volume. The province accounts for close to 40% of the national RPPI weighting, and Johannesburg alone accounted for 39% of all home loans processed through BetterBond in the 12 months to April 2026. In terms of sheer transaction activity, no other market comes close.

For estate agents: the data backs up what a strong referral network already tells you. Gauteng is a volume market. The Western Cape is a value market. Both are active, and both are worth being in.

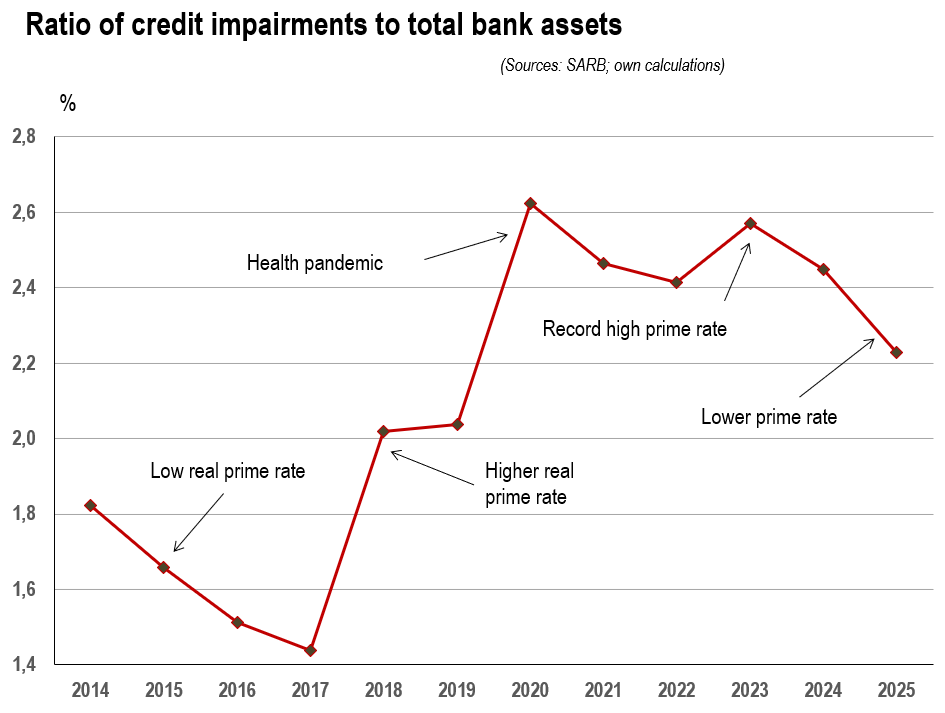

3. Banks are writing off fewer bad debts - a green light for lending

This one is a bit technical, but it matters. Banks track something called their "credit impairment ratio" - essentially, what percentage of their total loan book has gone bad (i.e., borrowers who stopped paying). When this ratio rises, banks get nervous and start tightening their lending criteria. When it falls, they tend to open the taps.

In 2023 and 2024, when interest rates were at record highs, South African banks saw a spike in loan write-offs. Households that had stretched to buy property during the low-rate environment of 2020–2021 started struggling. That's been well-documented, and it's one of the reasons home loan approval rates tightened significantly during that period.

The good news: as interest rates have started coming down through 2025 and into 2026, credit impairment ratios have followed. Banks are writing off less. That means improved appetite for new lending - which is directly relevant to home loan applicants.

For buyers: this is a meaningful tailwind. A healthier bank lending environment generally means better approval rates, more competitive interest rate offers, and greater flexibility on marginal applications. It's not a free pass - credit criteria still apply - but the tide is moving in the right direction.

4. Commercial vehicle sales point to growing economic confidence

This might seem like an odd one to include in a property article, but bear with us. New vehicle sales - particularly commercial vehicles - are a leading economic indicator. Businesses don't buy delivery bakkies and light trucks when they're nervous about the economy. They buy them when they're growing.

In the first quarter of 2026, commercial vehicle sales hit 47,500 units - the highest quarterly figure in over a decade. Total new vehicle sales for the first two months of 2026 were up 17.8% year-on-year to R45.7 billion. Light commercial vehicles (think one-tonne bakkies and panel vans) made up 84% of commercial sales.

What this tells us is that small and medium business confidence is returning. That has a knock-on effect for the property market: more business activity means more employed people, more income stability, and more creditworthy home loan applicants.

The big picture

Dr Botha's May 2026 report is, on balance, cautiously optimistic. The interest rate cutting cycle is underway, bank lending appetite is improving, the Gauteng and Western Cape property markets remain active, and business confidence is recovering. The main risk is external - global fuel prices driven by Middle East conflict - and that's largely outside anyone's local control.

For buyers sitting on the fence: the conditions are improving, and waiting for "perfect" rarely pays off in property. For estate agents: the fundamentals support continued transaction activity, particularly in Johannesburg and the Cape. And for existing homeowners: a declining impairment environment and a rate-cutting cycle are both working in your favour.

**Need to know where you stand?**Talk to Phoenix Bonds. We know the banks. The banks know us.